Canara Bank bags Skoch Award Canara Bank bags Skoch Award

March 23: Canara Bank has been awarded the SKOCH Award for Excellence in MSME Sector.

Mr Hemant Kumar Tamta, General Manager, Canara Bank Circle Office Delhi, and Mr K Virupaksha, DGM Head Office Bangalore, received the award from Mr Jayant Sinha, Minister of State for Finance.

Mr Sameer Kochhar, Chairman of SKOCH Group, was also present on the occasion.

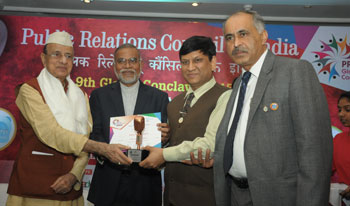

Canara Bank bags top PRCI Award

By Deepak Arora

NEW DELHI, March 14: Public Relations Council of India (PRCI) has conferred Canara Bank wity a top award in the Collateral Award Category. NEW DELHI, March 14: Public Relations Council of India (PRCI) has conferred Canara Bank wity a top award in the Collateral Award Category.

Former Tamil Nadu Governor Bhishma Narain Singh conferred the award to Canara Bank Delhi Circle General Manager Hemant Kumar Tamta and the Bank's Head Office DGM S T Ramachandra at an award ceremony here here on Saturday.

Present on the occasion were noted educationist Narendra Jadhav.

Public Relations Council of India (PRCI) is a national Registered Corporate Body, a Pan-India Organization of Public Relation Professionals, Corporate Communicators, advertising & media professionals and academicians.

The PRCI Annual Corporate Collateral Awards are the most prestigious event in the realm of corporate communications presented annually to recognize talent and professional standards.

The jury consisted of eminent professionals from the world of mass communication/ media. This year the PRCI received more than 750 nominations from 57 companies in 30 categories.

Canara Bank organises retail utsal in Delhi Canara Bank organises retail utsal in Delhi

NEW DELHI, March 14:

Canara Bank Delhi Circle Office organized a Retail Utsav at Bhagwan Das Road here on Saturday.

General Manager from Head Office MG Ajayan and General Manager of Delhi Circle Hemant Kumar Tamta along with other Executives of the Bank handed over sanction letters to a number of Beneficiaries.

Government appoints EDs of Canara, 8 other banks

NEW DELHI, March 11: The government has appointed executive directors at nine public sector banks (PSBs), including Canara Bank, Allahabad Bank, Bank of Baroda (BoB) and Bank of India (BoI). Harideesh Kumar B, a GM with Vijaya Bank, took charge as ED at Canara Bank.

R P Marathe, a general manager with BoB, is new executive director at BoI. Bank of Baroda said K Venkata Rama Moorthy, its GM, had been elevated as ED. Kishore Piraji Kharat, another GM at BoB, moves as ED to Union Bank of India. N K Sahoo, a GM at Canara Bank, is a new ED at Allahabad Bank.

Late last December, a government-appointed selection panel had interviewed 35 candidates to fill vacancies of 15 EDs in various PSBs. Of those interviewed, names of 15 were shortlisted and 12 were allotted to banks. However, a formal notification was pending.

Earlier, this year the government split the post of chairman and managing director at state-run banks, making each into two charges, one of chairman and the other termed managing director and chief executive officer. It then appointed MD & CEOs for United Bank of India, Oriental Bank of Commerce, Vijaya Bank and Indian Overseas Bank.

Last month, it had also said the existing appointment methods for the top posts would be scrapped and candidates from the private sector would be aligible, too, to be interviewed.

Harideesh Kumar B, who took charge as Executive Director of Canara Bank on Wednesday, hails from Dakshina Kannada district of Karnataka. He is a Post Graduate with a Degree in Law and started his Banking career with Vijaya Bank in the year 1978.

He has worked in various capacities in the Bank across the country. His distinguished career of 38 years spans across Goa, Kolkata, Mumbai, Ahmedabad, Bangalore and Delhi. He has worked in various operational areas of banking and is a knowledgeable and able administrator.

He has headed Vijaya Bank’s Regional offices at Chandigarh, Bangalore and Delhi. He was heading Vijaya Bank’s Delhi Region as General Manager prior to joining Canara Bank as Executive Director.

Arun Jaitley stepped out and hit a six in his first budget

NEW DELHI, March 1: In ideal circumstances, reforms and policy-making should not be linked to a calendar event such as the Union budget. Yet sometimes, it is useful to use the budget as a platform to announce, in unequivocal terms, the government’s blueprint for development. Rarely in recent times has the overhang of anticipation been so heavy in the run-up to the budget as this year.

By all measures, this is probably the last budget as we know it. If things work to plan, India’s finance minister will have ceded a significant part of his discretionary power over indirect tax rates by the time the next budget is presented. A single tax on goods and services across the land would be set by a collegium of ministers from the states. Besides, the 14th Finance Commission recommendations of sharing 42% of central tax revenues with states had made the elbow room in the treasury that much tighter. Union finance minister Arun Jaitley thus had to scour for that extra rupee to be wrung out of the coffers to balance the books.

By incentivising household financial savings, tax breaks for a host of sectors to push manufacturing and job creation, and raising the service tax rates to 14%, Mr Jaitley is ushering in a new era in India’s tax architecture. Shifting the incidence of tax from income to consumption, and goading deeper financial savings, the minister has assumed that the resultant investment, should also nurse the recovery along with improving the fiscal balance. The risk in this gambit is to the price line as producers pass on the higher tax.

The regime change also envelops a calibrated roll-out of a new development framework. Even though overall subsidies are stubbornly stuck at 13.17% of total government expenditure, the minister has also laid out a roadmap for reforming India’s infamously porous welfare handout regime to make it more efficient.

Bureaucrats and economists may love shooting down subsidies because they bloat the fiscal deficit and burden the government but the simple fact is that in a one-billion strong nation, in which nearly one in every three live below the poverty line, one needs an efficient method through which privileged tax payers can support the poor.

As welfare entitlements become legally enforceable, the onus will be on cutting back revenue expenditure. Mr Jaitley’s plan for 2015-16 is aimed at keeping subsidies at less than 2% of gross domestic product (GDP). The government’s argument: It is critical to bring down expenditure that do not yield intended objectives.

Equally, the finance ministry’s zeal is directed more towards pruning the fiscal deficit. One in three rupees Mr Jaitley spends in 2015-16 will be borrowed, a prospect the bond market could greet with some degree of trepidation. With inflation the foremost concern, the cost of fiscal consolidation could also be pretty high. For now, he has stuck to the broad medium-term fiscal policy roadmap and pegged the fiscal deficit at 3.9% of GDP in 2015-16. Accomplishing this goal is based on two basic assumptions: Tax revenues will grow by 15% in 2015-16 compared to the previous year; and non-tax revenues will yield expected earnings of Rs 221,732.59 crore. Mr Jaitley has dipped into receipts like divestment and spectrum auction proceeds to help shave 0.2 percentage point off the fiscal deficit, but the risk is that these revenue streams are not in perpetuity and cannot be a substitute for expenditure control.

The stock markets found cheer in lower corporate tax rates, although analysts said effectively the tax outgo for companies actually would have gone up. Investors would have preferred more clarity on the retrospective tax laws. Investment decisions, besides yields and returns, are also guided by perception. Foreign direct investment (FDI), apart from bringing in the crucial dollars, also plays an ambassadorial role. Seen through the prism of trans-continental conduct, corporate giants are akin to global citizens helping countries reap the benefits of comparative and competitive advantage. Investors wanted a complete roll-back on the retrospective taxes on corporate acquisitions. The minister stopped short of it, but said it will be imposed only sparingly.

He announced plans to enact a law to deal with India’s infamous and bustling parallel economy. But the government should be careful that the new law is robust enough and not prone to misuse

Mr Jaitley probably was also acutely conscious of the fact that India needs to propel the investment rate to over 40% of GDP. He did not wield the knife to cut capital expenditure, which as a proportion of the Centre’s total spending has been pegged at Rs 24,1430 crore, or 13% of the Rs 17.7 lakh crore budget in 2015-16, from 11.4 % in 2014-15.

If the last nine months were about proof of concept through a raft of new initiatives such as Make in India, Jan Dhan, and Swachh Bharat, the next 12 months could be about proof of delivery. Half-measures tend to linger and time was fast running out. So, this was just the right moment for taking ‘gut’ decisions for the economy to accelerate. There were enough signs in Mr Jaitley’s first full budget that he was willing to come out of the crease and hit a six.

Indo-US Merchandise & Services Trade To Touch US$ 525 b By 2025

NEW DELHI, Feb 25: PHD Chamber of Commerce and Industry has projected that Indo-US bilateral trade in merchandise as well as services sector is likely to go up to US$525 billion by 2025 in view of recent bilateral policy measures undertaken by the two democracies of the globe.

The report named “India-USA Economic Relations” which was jointly released here today by Washington State Department of Commerce and PHD Chamber, however clarifies, “Indo-US merchandise trade has potential to accelerate to a level of US$325 billion in next ten years whereas prognosis for two nations services trade are estimated at US$200 billion for 2025.

The report has been released on the occasion of an Interactive Session on “Expand Your Business in North America” under aegis of by PHD Chamber here today in which Assistant Director, Washington State Department of Commerce Ms. Mary Trimarco and President PHD Chamber Mr. Alok B. Shriram took part expressing confidence that with recent bilateral policy measures taken by the US administration and the Indian government such as Indo-US Nuke deal, extension of their defence pact for another 10 years as well as forging closer partnership for developing smart cities in India, would further cement the Indo-US trade and economic ties to achieve the forecast.

The release of report was also witnessed by Minister Counselor for Commercial Affairs US Commercial Service, US Embassy in India Mr. John M. McCaslin, Chairman, International Affairs Committee of PHD Chamber Mr. Deepak Pahwa, its Secretary General Mr. Saurabh Sanyal and Senior Corporate Vice President and Chief Productivity and Competitiveness Officer of HCL Technologies Mr. Rajiv Sodhi.

According to official estimates, the Indo-US merchandise trade stood at US$63 billion whereas their service trade is calculated at US$34 billion during fiscal 2013-14. Both the merchandise trade as well as services trade between India and US in totality was calculated at US$97 billion.

The report further points out that in the light of recent positive outlook towards strengthening bilateral economic relations, it is imperative on the part of both India and US to frame the strategies in such a way so that these initiatives can well be executed at the ground levels; effective benefits can be derived out of these relations, untapped potential can be harnessed and economic relations between the two can be strengthened in coming times.

SIAL China to help boost Food & Beverage trade ties with India

By Deepak Arora

NEW DELHI, Jan 21: SIAL China, Asia’s largest food & beverage show, will be held in Shanghai from May 6 to 8. The 2015 edition of SIAL China will be attended by 2700+ exhibitors and 55,000+ visitors from all over the world. NEW DELHI, Jan 21: SIAL China, Asia’s largest food & beverage show, will be held in Shanghai from May 6 to 8. The 2015 edition of SIAL China will be attended by 2700+ exhibitors and 55,000+ visitors from all over the world.

Making an annoucement here on Wednesday, the officials said that there was increasing momentum in Indo-China trade relations and it offered new opportunities for furthering Food and Beverage trade between the two neighbors.

Addressing the newsmen, Director General of the Chindia Chamber of Commerce Tribhuvan Darbari, gave a macroeconomic overview of Indo-China relations. Touching upon the recent visit of Chinese President Xi Jinping to India, Darbari said that relations between India and China are gathering momentum across a variety of spheres, including economic development, urban cooperation, audiovisual co-production, drug standards, cultural co-operation and railways.

The Director General stated “the trade between the two countries will be over USD 60 billion this year, up from USD 270 million just 20 years ago.”

Darbari said “F&B industry is one of the fastest growing sectors in the world and supporting a platform such as SIAL China is a step in the logical direction for India and China.”

Minister and Deputy Chief of Mission from the Embassy of the People’s Republic of China Yao Jing said that India and China have a long history of bi-lateral trade. He invited the two countries to “reopen the old Silk and Spice routes. This can be done with modern-day products such as agricultural commodities and processed food.”

He added that “China is not only a provider of manufactured goods but also a provider of goodwill. We invite Indian food processors and importers across the board to participate in SIAL China. Indian companies will be very competitive in the Chinese market and we would like to see them develop their presence in China.” He added that “China is not only a provider of manufactured goods but also a provider of goodwill. We invite Indian food processors and importers across the board to participate in SIAL China. Indian companies will be very competitive in the Chinese market and we would like to see them develop their presence in China.”

Director of the North East Asian Desk at the Department of Commerce Sanjeet Singh said that the balance of trade between the two countries weighs heavily in favour of China. “This trade deficit is a major cause for concern for the Indian government. However, currently there is a renewed vigour and focus on developing bilateral trade in goods, services and also in investments between the two neighbours. India needs to capitalize on the Make in India campaign and shift export focus from raw commodities to manufactured and processed goods.”

He also added “The Indian government is keen to exchange with China across the board. We are happy to see events like SIAL China being promoted in India and we will be happy to provide the policy support required to further the development of F&B trade between India and China.”

Exhibition Director of SIAL China Bjoern Kempe explained that China is world’s largest consumer market and its food market is forecast to exceed 1.5 trillion USD by 2016.

“Chinese are savvy consumers and are interested in products that are high quality, exotic, safe and novel. Dairy products, vegetable oils, Livestock and poultry and seafood are some of the major Chinese food imports. As a developing agricultural production powerhouse, India is well positioned to supply China for its import needs in meat, seafood, dairy, fruit pulps, cereals and value added food.”

The SIAL Innovation area builds on the 50 years of SIAL Group experience in identifying cutting-edge food trends and showcasing them at SIAL Group exhibitions across the globe: in Canada, Brazil, France, Middle East, China, Philippines and Indonesia.

At SIAL China, the SIAL Innovation display will present prize-winning food and beverage products that embody the hottest upcoming trends in the Asian F&B industry.

Kempe explained that “in addition to these innovative products, Indian visitors will be able to discover gourmet products from a range of 55 countries participating at the SIAL China, such as Thailand, Indonesia, Malaysia, Japan and Korea.”

MK Parimoo and Rajesh Sharma from the Trade Promotion Council of India (TPCI), organizers of the India pavilion at SIAL China, shared their experience of participation at the exhibition. They mentioned that SIAL China is an excellent platform for promoting Indian F&B products not only to the Chinese market but also to access buyers from across Asia.

Parimoo pointed out “In F&B, our strengths are bovine meat, marine products and dairy products to a certain extent.”

Sharma reminded the audience that the SIAL China India pavilion 2015 is open for registration and interested companies may contact TPCI.

The discussion was followed by a networking lunch where attendees had the opportunity to further discuss issues relating to Indo China relations and the Food and Beverage industry. All professionals agreed on the huge potential provided by the SIAL China platform – it is a great international business platform for Indian F&B visitors and exhibitors to promote their products and services at Asia’s biggest marketplace.

Oil price will average less in 2015 than during financial crisis, survey finds

NEW YORK, Jan 31: Crude oil will likely continue falling before posting only a mild recovery in the second half of this year, a Reuters survey of analysts showed on Friday, with prices set to average even less in 2015 than during the global financial crisis.

The survey of 33 economists and analysts forecast North Sea Brent crude would average $58.30 a barrel in 2015, down $15.70 from last month's poll, in the biggest month-on-month forecast revision since prices last collapsed in 2008-2009.

If the forecasts for 2015 prove correct prices will average the lowest since 2005, even if they recover after June, illustrating the impact of Opec's decision to maintain output in the face of fast-growing US shale output.

"It should be a year of differing halves. The likelihood of further near-term fund selling will see Brent trade down to $42 per barrel and WTI at $40 per barrel by the end of Q1 2015," ANZ analyst Mark Pervan said.

"The mood will remain cautious for the remainder of the first half of the year, before high-cost US supply discipline starts to emerge in the third quarter," he added.

Twenty seven of the 28 analysts who contributed to data for both the December and January Reuters polls have slashed their forecasts. More than half of those lowered their projections by $15 a barrel or more from last month.

European investment bank Barclays, which has the lowest forecast according to the poll, cut its 2015 price outlook for Brent by almost 40 percent to $44 per barrel.

Goldman Sachs, widely-seen as one of the most influential banks in commodity markets, sees WTI hovering around the $40 per barrel mark for much of the first half of this year. It has slashed its 2015 Brent forecast by $33.40 to $50.40 per barrel.

Most of the analysts were in agreement that the Organization of the Petroleum Exporting Countries (Opec) would maintain its stance of not cutting production despite oil prices touching multi-year lows, with any tightening of supplies expected to come from higher-cost producers outside the group.

"Low crude prices negatively affect (US) shale oil profitability," Intesa Sanpaolo analyst Daniela Corsini said.

"I expect to see lower rig counts and lower investments over the next months ...before the end of the year, shale oil supply should start contracting."

Brent has averaged $49.57 so far in January, consolidating over the past two weeks after hitting a near six-year low of $45.19 a barrel on January 13. It was trading around $48.75 on Thursday.

The poll forecasts US light crude will average $54.20 a barrel this year and $64.90 in 2016. WTI has averaged $47.24 a barrel so far in 2015, hitting a post-2009 low of $43.58 on Thursday.

Brent's premium to US crude, known as the Brent-WTI spread, is expected to widen to $4.10 a barrel in 2015 from around $2.20 so far this year, the poll showed.

That would be the smallest annual Brent-WTI average since 2010. Brent-WTI averaged more than $12.50 a barrel between 2011-2014 as the shale boom drove the US benchmark to a steep discount to its North Sea rival.

Canara Bank bags 3 MSME Awards Canara Bank bags 3 MSME Awards

By Deepak Arora

NEW DELHI, Jan 10: Canara Bank, a leading nationalized Bank, has bagged three awards at the annual Flagship event “MSME Banking Excellence Awards-2014” organized by Chamber of Indian Micro,Small & Medium Enterprises (CIMSME) here on Saturday.

Canara Bank has been adjudged as the “Best Bank Award-Winner” amongst other awards.

Union Minister for MSME Kalraj Mishra presented the awards. R Madhusudan, General Manager, MSME Wing HO, received the Awards. Hemant Kumar Tamata, General Manager, Delhi Circle, was also present on the occasion.

RBI cuts repo rate

NEW DELHI, Jan 15: The Reserve Bank of India (RBI) cut the repo rate on Thursday by 25 basis points to 7.75% in a surprise inter-meeting cut, yielding to growing signs of slowing inflation and a flagging recovery.

The RBI kept the cash reserve ratio unchanged at 4%.

The repo rate -- the rate at which banks borrow from RBI -- was under the liquidity adjustment facility (LAF), RBI governor Raghuram Rajan said.

The reverse repo rate under LAF stands at 6.75%.

Plunging global oil markets helped India post slower-than-expected wholesale price inflation in December, raising hopes for an early cut in interest rates to help the economy out of its longest phase of sub-par growth since the 1980s.

In a statement, the RBI cited lower-than-expected inflation, weak crude prices and weak demand, as well as the government's commitment to sticking to a fiscal deficit target.

"These developments have provided headroom for a shift in the monetary policy stance," it said.

The wholesale price index for December, released on Wednesday, rose just 0.11% year-on-year compared with a 0.6% jump forecast by economists in a Reuters poll.

Wholesale prices were unchanged in November.

Modi promises easiest doing business in India

AHMEDABAD, Jan 9: Prime minister Narendra Modi on Sunday discussed counter-terror cooperation, among other issues such as greater economic ties, with senior leaders of the US and Canada visiting India for the Vibrant Gujarat Summit here.

In his meeting with the US secretary of state John Kerry, discussions primarily focused on the upcoming visit of US president Barack Obama and issues like counter-terror co-operation, while economic matters and matters of regional interest also figured in the talks.

“Both sides agreed that the visit would add momentum to the India-US strategic partnership. They also noted that issues relating to WTO Trade Facilitation had been satisfactorily resolved,” an official statement from the Prime Minister’s Office said.

Counter-terror cooperation was also a key theme in the prime minister’s meeting with Canada’s Minister of Citizenship and Immigration Chris Alexander.

“The prime minister condemned the attack on Canada’s Parliament, and stressed the need for a zero-tolerance approach to terror,” the statement said.

Modi also said he looked forward to visiting Canada.

Besides, Modi met Israel’s Agriculture Minister Yair Shamir and both sides sought to further enhance cooperation in the agriculture sector.

The Prime Minister invited Israel to take advantage of the Make in India initiative and establish high-end manufacturing centres in India. In Modi’s meeting with Akbar Torkan, senior advisor to the president of Iran, both sides reviewed progress in the implementation of the Chahbahar Port Project. Energy cooperation and regional issues also came up for discussion.

Separately, Modi also met World Bank president Jim Yong Kim wherein climate change and clean energy came up for discussion. In his meeting with the Prime Minister of Macedonia, both sides agreed on the need to enhance trade and investment ties. The governor of Astrakhan, Russia, Alexander Zhilkin, invited investment from India in his meeting with Modi.

Companies commit 2 lakh crore

Big corporates — including Ambanis, Adanis and Birlas as also Suzuki and Rio Tinto from abroad — on Sunday committed to investing about Rs2 lakh crore and creating more than 50,000 jobs, as prime minister Narendra Modi promised to make India the ‘easiest’ place to do business with a stable policy and tax regime.

Modi also promised truly unlimited development across sectors and regions, while business leaders lined up huge investment commitments and signed 31 MoUs across sectors on the first day of the three day Vibrant Gujarat Summit (VBS).

Addressing an audience, with US secretary of state John Kerry, UN secretary general Ban Ki-moon and World Bank president Jim Yong Kim and top CEOs in attendance, Modi expressed government’s commitment to creating a policy environment that is predictable, transparent and fair and a stable tax regime.

“Ease of doing business in India is a prime concern for you and for us. I assure you that we are working very seriously on these issues. We want to make them not only easier than earlier; not only easier than the rest; but we want to make them the easiest,” he said, seeking to address concerns of investors with regard to red tap and problems that had emanated from retrospective tax amendment of the previous UPA government.

Participating in the deliberations, several CEOs made lavish investment commitments.

Reliance Industries chairman Mukesh Ambani announced Rs 1 lakh crore investment across businesses in the next 12-18 months in the state, while Aditya Birla Group chief Kumarmangalam Birla promised to pump in Rs20,000 crore over a period of time to ramp up capacities across various existing facilities.

Adani Group and US-based SunEdison committed to investing Rs25,000 crore for solar park and Welspun Renewables announced Rs8,300 crore to set up about 1,000 MW solar and wind capacities in Gujarat. Commitments were also made by other business houses like Kalyani Group.

Hong Kong-based China Light & Power Holdings Ltd is planning a 2000 Mw coal-based power plant in Gujarat. The project cost is estimated at around USD 2 billion (approximately Rs 12,400 crore).

On Saturday, wind turbine maker Suzlon had committed Rs 24,000 crore over 5 years to generate 3,000 mw in Gujarat.

Modi praises IFFCO in one-to-one meeting with Dr U S Awasthi

By Deepak Arora

NEW DELHI, Dec 31: Dr U S Awasthi, CEO and Managing Director of IFFCO (Indian farmers Fertiliser cooperative Limited), world’s largest cooperative society in processed fertilisers sector, met Prime Minister Narendra Modi on Wednesday at his office. Dr Awasthi shared his experiences, understanding and appraised him about IFFCO, Cooperatives, Agriculture and Rural India. NEW DELHI, Dec 31: Dr U S Awasthi, CEO and Managing Director of IFFCO (Indian farmers Fertiliser cooperative Limited), world’s largest cooperative society in processed fertilisers sector, met Prime Minister Narendra Modi on Wednesday at his office. Dr Awasthi shared his experiences, understanding and appraised him about IFFCO, Cooperatives, Agriculture and Rural India.

Prime minister Narendra Modi expressed his admiration for IFFCO, which has become the world's largest cooperative society, and its praiseworthy performance as a leading source of fertilisers to farmers in the country.

Immensely impressed by the persona of Modi, Dr Awasthi described in his tweets the Prime Minister as humble, dynamic, inspiring and innovative leader.

In his tweet, Dr Awathi said: “The aura of @narendramodi ji glides you along with him. Indeed a dynamic, simple, humble & quite inspiring #leader. An innovator & motivator.”

Dr Awasthi discussed issues such as direct transfer of subsidy to farmers, Jan Dhan Yozana, Swachh Bharat Abhiyan and social forestry as well. He tweets “Disc. #JanDhan, #IFFCO social #forestry #farmer dev. & #SwachhBharat. Very upbeat & happy after meeting the visionary PM @narendramodi Ji.”

The IFFCO Managing Director also discussed about soil nutrition and making the soil more productive by using balanced approach of fertilisers.

In his tweet, he said “Explained @narendramodi Ji abt #IFFCO’s efforts in promoting Green Manure, #Compost & #Soiltesting in fields 4 good yield & better soil health.”

He appriased the Prime Minister about Save The Soil Campaign of IFFCO which is constantly improving soil fertility wherever it is implemented till date.

Dr Awasthi also informed the Prime Minister about growth and scope of cooperatives in country and shared that now IFFCO has become the world's number one cooperative in the world.

Dr Awasthi also appraised the PM about excessive use of Urea by farmers, which is actually hurting the soil productivity.

In his tweet Awasthi said: “Also informed PM about the excess use of #urea and how it’s affecting our #soils. #NBS is the need of the hour to save soil and inc. prod.”

IFFCO becomes World’s Number One Cooperative; Crosses Rs 1,000 cr profit: Dr U S Awasthi

Contributes towards PM’s ideas of Clean India, Make in India, Jan Dhan Yojna

By Deepak Arora

NEW DELHI, Jan 1: From being first to contribute towards visionary Prime Minister Narendra Modi’s ideas of a clean India (Swach Bharat Abhiyan), financial inclusion (Jan Dhan Yojna) and domestic manufacturing (Make in India), Asia’s largest Cooperative IFFCO has become Number One Cooperative of the world in the year 2014. Besides commencing its production and operation of Jordan joint venture, IFFCO has already Rs 1,000 crores profit, informed Dr U S Awasthi, its Managing Director. NEW DELHI, Jan 1: From being first to contribute towards visionary Prime Minister Narendra Modi’s ideas of a clean India (Swach Bharat Abhiyan), financial inclusion (Jan Dhan Yojna) and domestic manufacturing (Make in India), Asia’s largest Cooperative IFFCO has become Number One Cooperative of the world in the year 2014. Besides commencing its production and operation of Jordan joint venture, IFFCO has already Rs 1,000 crores profit, informed Dr U S Awasthi, its Managing Director.

In his New Year message, IFFCO Managing Director Dr U S Awasthi said “the International Cooperative Alliance (ICA) recognized our efforts and in its report titles “World Cooperative Monitor 2014” ranked IFFCO as the No. 1 cooperative amongst the top 300 cooperatives in the World today (GDP per capita basis).”

He also announced that due to sound financial management and expenditure management by our finance team along with the efforts of over 6000 plus work force and the directions of an able board members we have already crossed Rs.1000 crores profit.”

Dr Awasthi also shared with his employees the happy news that IFFCO’s Joint Venture project in Jordan has formally started its production and operation. It has also achieved financial closure of around $860 million.

He said IFFCO has begun contributing towards visionary Prime Minister Narendra Modi’s ideas of a clean India (Swach Bharat Abhiyan), financial inclusion (Jan Dhan Yojna) and domestic manufacturing (Make in India).

“We have pledged Rs.10 Crores towards the Swach Bharat Abhiyan. Our employees and our 39,000 cooperative societies are doing their bit by keeping their surroundings clean and healthy and inspiring everyone around them to do so. We are also through our dense network in India appealing to common citizens to open a bank account and are leaving no stone unturned in ensuring that anyone and everyone connected with IFFCO have a bank account.”

Dr Awasthi said “2014 will be remembered as a significant year not only for the politics but also for the socio economic set up of this great country. We witnessed the largest democratic exercise in the world produce one of the most stable government. India has seen in many decades, beckoning hope for billions.” Dr Awasthi said “2014 will be remembered as a significant year not only for the politics but also for the socio economic set up of this great country. We witnessed the largest democratic exercise in the world produce one of the most stable government. India has seen in many decades, beckoning hope for billions.”

“Not only India but the World has changed more in the last year then it did for many years together. As a responsible and a professionally managed farmer cooperative, IFFCO is taking pro active steps to match up to the pace of change that takes place all around us. This requires us to innovate and also contribute to new ideas. We believe that it is our duty to match steps with the visionary who is now leading us into the future.”

Dr Awasthi said “IFFCO not only makes in India, but makes for India as well. Our five state of the art fertilizer manufacturing units produce the best quality fertilizers for the Indian farmers, something that we are immensely proud of. All our business decisions and overseas acquisitions aim at making in India and making for India.”

Wish all a very happy new year and prosperous new year 2015, the Managing Director said another piece of news that came from ICA was the election of Aditya Yadav on the ICA global board. The election of Yadav, who is also a member of the IFFCO Board, ensured that India has a say on the most powerful global platform for the cooperative sector.

While back home, he said the elections for the IFFCO Board were the most talked about in the Indian Cooperative sector. It was a one of its kind “cooperative democratic” exercise in India and was lauded for its transparency, peaceful conduct and moreover, the importance it gave to its women members.

IFFCO produced around 56.60 lakhs MT till December 2014. Though the production was affected this year due to policy matters and minor technical snags, but we are still able to produce to the best of our abilities.

Although there were piling inventories and unconducive market conditions but despite that our marketing team was able to register sale dos around 80 Lakh MT, which is better than what we achieved last year.

He said that due to sound financial management and expenditure management by our finance team along with the efforts of over 6000 plus work force and the directions of an able board members we have already crossed Rs.1000 crores profit.

For these startling efforts by our dedicated workforce IFFCO won various laurels at national and international platforms. Our production and marketing teams won over ten FAI awards this year in various categories of Production, Energy Saving, Environment Protection, Marketing, use of ICT in Agriculture amongst others.

The Managing Director said “we have temporarily suspended our plans of the Urea project in Quebec, Canada due to cost overruns. Our partners are in agreement with the decision of the temporary hiatus and we will restart the project at favorable time. Besides this both IKSL and IFFCO Tokio General Insurance along with other joint ventures are on track and doing well.”

The year gone by has taught us some valuable lesson in cooperation, teamwork, knowledge sharing and adaptability. It has taught us to be always be geared for change and we can only achieve this by equipping ourselves with latest trends in organizational management and also in technology.

Dr Awasthi said “2015 will be a year when we set new milestones for ourselves. We will together work towards a vision 2020.”

He said the year 2015 will also be celebrated as International Year of Soils, as declared by 68th UN General Assembly. It is my request to you all to promote the slogan of “Healthy Soils for Healthy Life”. IFFCO is doing its bit to make it happen through our “Save the Soil” campaign, which is running successfully across the country. Let’s work together to promote balanced use of fertilizers and conserve the environment.”

Krishna Kumar opens 700th ATM of Canara Bank in Bengaluru Krishna Kumar opens 700th ATM of Canara Bank in Bengaluru

BENGALURU, Jan 5:

Mr V S Krishna Kumar, MD & CEO of Canara Bank, inaugurated the 700th ATM of Bengaluru Metro Circle at HPCL Venkatadri Station, Banaswadi Main Road here here on Monday.

The function was attended Mr S S Bhat, Chief General Manager, Mr Ravindra Bhandary and Mr M A Nayagam, General Managers, besides executives from Head Office and Circle Office.

Canara ED Krishana Kumar opens 40th Shikhar branch in Delhi

By Deepak Arora

NEW DELHI, Dec 31: Canara Bank Executive Director Krishana Kumar inagurated the bank's 40th Shikhar branch here at Dwarka on Friday. NEW DELHI, Dec 31: Canara Bank Executive Director Krishana Kumar inagurated the bank's 40th Shikhar branch here at Dwarka on Friday.

Delhi Canara General Manager Hemant Kumar Tamta, Circle executives and branches head along with customers were present on the occasion.

Project Shikhar is a transformation aimed at enabling the bank to effect the changes to enhance performance in terms of key parameters viz CASA, robust credit growth, fee income, number and proportion of e-transactions and asset quality and reovery to scale to the top ie the Shikhar, according to Krishana Kumar.

The Executive Director expressed happiness while inaugurating the 40th Shikhar branch over the re-engineered branch under the project with features like welcome desk, queue management system, single window operator system and daily staff meetings to boost customer experience and drive higher sales.

EU hopes to seal free trade pact with India next year

MUMBAI, Dec 14: The Free Trade Agreement between India and the European Union is expected to materialise next year once the country finalises its new foreign trade policy, a top official has said.

"We are actually not very far from the agreement but we are not there yet. I am quite positive that next year or so it would be possible to finalise the free trade agreement," said EU Ambassador Joao Cravinho.

He said parties on both the sides are engaged in good political conversations and there has been a commitment from both the sides on finalising the FTA.

However, this is yet to be translated into actual progress in negotiations, Cravinho said on the sidelines of the 22nd annual general meeting of the Council of EU Chambers of Commerce here over the weekend.

"The Indian government has been a little slow; slower than we wanted to, in producing the new trade policy," the envoy said, but added that as the trade agreements last for as long as 15-20 years, a delay of a few months in policy formulation is not relevant.

Commerce and Industry Minister Nirmala Sitharman had in September said that the new five-year FTP would be different from the previous ones and hopefully announced soon. The policy is expected only from April next.

Earlier, the government had planned to introduce a new FTP immediately after the Budget in July but it has been delayed reportedly on account of some tax related issues between certain ministries.

"We expect that in the new year we will see a new trade policy. Once that happens, we will be able to sit down again and resume our negotiations," Cravinho added.

The EU is open for an asymmetrical agreement, he said, adding, however, that both sides must be agreeable for a little bit of give and take.

He pointed to the difference in taxation on cars imports from Europe as opposed to cars being exported.

Cravinho said: "We understand India's growth imperative and are keen to have a very positive interaction. And so the agreement will be asymmetrical. At the moment, tariff (on cars imported from Europe) is up to a 100 per cent, whereas the duty on car shipped to Europe is only 7-8 per cent."

He added: "We are not saying they have to be equal on both sides but they should be proportionate...taxation has to come down quite significantly."

India ships 2,00,000 cars to Europe each year while Europe exports about 40,000 cars to India, he said.

Cravinho said he is optimistic about growth in India, which is currently at a level well below its potential as an investment destination than many of its competitors.

"In my conversation with EU business leaders, and we share the optimism (on India), there is also very much a recognition that the environment for investment has not yet changed significantly. There has been some change but it is more of a psychological than substantive nature," he said.

The government needs to improve the investment climate further, leading to increased inflows that will help build the country's manufacturing capacity, he added.

Talking about the 'Make in India' initiative, Cravinho said it reflects the government's ambition and will also help the country enter the global value chain.

He also said the last year's ban by EU on India's Alphonso mangoes is likely to be lifted soon.

Right time to free, unshackle fertiliser sector: Dr Awasthi

NEW DELHI, Dec 15: With the wholesale price inflation hitting zero in November, its slowest level since July 2009, Dr U S Awasthi, Managing Director of world's biggest Cooperative IFFCO, has said this was the right time to free and unshackle the fertilizer sector. NEW DELHI, Dec 15: With the wholesale price inflation hitting zero in November, its slowest level since July 2009, Dr U S Awasthi, Managing Director of world's biggest Cooperative IFFCO, has said this was the right time to free and unshackle the fertilizer sector.

IFFCO's Managing Director, Dr U S Awasthi, in his tweet said “#WPI #Inflation touching 0% for this month is an easing gesture for our #economy. The right time to free & unshackle #Fertiliser Industry.”

The fuel inflation dropped to a five-year low and the rate of price rise in food items fell drastically due to favourable bases and declining global commodity prices, the official data released on Monday showed.

The RBI Governor Raghurajan Ram who has been playing too cautious, is under pressure from all sides to ease the rate.

With retail inflation having hit a fresh low of 4.38% in November and industrial production at a three-year low in October, the latest wholesale price index (WPI) inflation data pile on the pressure on the Reserve Bank Of India (RBI) to effect the much-anticipated rate cut to boost the economy.

Recently, the Reserve Bank of India breathed fresh life into infrastructure projects by allowing flexible financing options for existing projects in the infrastructure sector and heavy industry.

On similar lines the fertilizer sector which is heavily dependent on import has been demanding policy reforms to tackle the situation.

In the recently concluded seminar organized by the fertilizer producers of the country in Delhi, the Union Minister Anant Kumar was briefed about the macro-issues plaguing the sector.

With news of dipping inflation doing rounds, the IFFCO Managing Director has renewed his demand.

India the 'brightest spot' in sluggish Asia Pacific economy: S&P

WASHINGTON, Dec 9: Ratings agency Standard & Poor’s (S&P) has called India the only bright spot in the Asia Pacific region in an otherwise shaky finish to year 2014 with all other economies losing momentum.

“Only India is bucking the trend,” said S&P in a report on Asia Pacific region’s credit outlook released on Tuesday. “India has been the region’s brightest spot,” it added.

The reason for its sunny outlook for India was PM Narendra Modi’s government that, the agency said, has picked up the pace of reform after a “modest” start.

This marks a sharp turnaround about India’s image as an investment destination among overseas analysts who had been unsparing about their criticism of the previous UPA government’s management of the Indian economy, hit by a policy standstill, corruption scandals and tax disputes.

The agency said that while China’s economy continues to slow, Japan is in “technical recession” and trade-dependent economies continue to suffer from lack of external demand.

Asia’s third-largest economy is showing signs of clawing out of its longest slump in a quarter century, and the raft of measures that Modi has announced has raised hopes that the government will be able to engineer a quick turnaround.

The government has vowed to remove red tape, ease rules, and pledged a non-adversarial governance regime to push companies to make India a manufacturing powerhouse through initiatives such as `Make in India’.

S&P upgraded India’s credit rating to “stable” from “negative” in September, by which time most of Modi’s announcements and measures were under way in various forms and stages.

The agency proceeded to list them: ending diesel subsidy, liberalizing foreign investment in insurance, and controlling discretionary government spending.

The agency also noted some of the programmes announced by Modi — financial inclusion by opening bank accounts for 100 million people who didn’t have one, streamlining government-transfer payment regimes, improving rural infrastructure, and cutting the number of government departments.

S&P welcomed the decision for “eliminating the planning ministry”. In August, Modi had announced the government’s intent to replace the Planning Commission with a new body, bringing the curtains down on the 64-year old institution founded on former Soviet Union’s command-style development model.

“Confidence has improved and growth momentum is now at around 7%,” said the agency, adding, however, a note of caution: “the build-up of corporate, and in some cases household, debt over the past five years remains a significant ‘tail’ risk,” S&P said on Tuesday.

The World Bank said in June that the India is already “benefiting from this ‘Modi dividend’ … with economic activity buoyed by expectations from the newly elected government”.

PM’s foreign visits helped India perception as top investment destination: ASSOCHAM cross-country survey

NEW DELHI, Dec 7: Prime Minister Mr Narendra Modi’s visits to the US, Australia and Japan among other countries has helped significantly change India’s perception as a promising and stable investment destination among global investors, 77 per cent of the respondents in ASSOCHAM’s survey of trans-national companies said.

The perception survey was done by ASSOCHAM’s newly opened foreign offices including in the US and Australia sensing the mood of the multi-national companies which have either already established presence in India or are seriously considering looking at India.

“Over 71 per cent of the senior level functionaries of these firms said that India tops the chart among the emerging countries as an investment destination. As many as 53 per cent said that India could even overtake China as an investment destination in terms of growth potential,” the survey said. China is slowing while India will catch up fast, it noted.

An overwhelming 89 per cent of the respondents said it is the leadership in India which has made all the difference in the perception of global investors, helped by continuous domestic growth story.

“There was an across-the-broad consensus about the Prime Minister Mr Narendra Modi being a very good communicator and who is able to establish a contact with the global community with as much ease as he is able to do at home,” it said.

Equally important was their observation about the credibility of his promises. “Over 73 per cent of the 161 respondents spread across the US, Japan, Australia, Singapore , Malaysia and the Middle East said Mr Modi will be able to deliver on his promises on ease of doing business, improving basic infrastructure and on debottlenecking the policy issues”.

His attention to small details and capacity to take decisions quickly was something which stood out in the survey reports from different regions. “There was a lot of appreciation in the US they way Mr Modi ironed out differences with the US on the issue of WTO agreement on trade facilitation and food security."

Mr Modi’s intense engagement with the NRI communities in the US and Australia has resulted in the Indian expats becoming the brand ambassadors of the country’s revival path.

In Japan, the points most noted about the Prime Minister’s leadership were his priorities to infrastructure projects, including modernization of the Railways. Bringing in of Mr. Suresh Prabhu, who has established an image of being a doer, in the Railway Ministry, was noted particularly in Japan, Singapore and Australia.

The ASSOCHAM reports from Australia indicated that the companies based in Australia want to build on the Prime Minister’s flagship programmes of smart cities, cleaning Ganga and improving urban infrastructure.

“The message that went about across different countries was that the new government in New Delhi wants to engage widely with the world, spreading the message of India story. The results would be there in much more visible form in the next few months. However, the results in the financial markets are already visible in terms of the sensex touching new highs on the back of foreign inflows. While dollar is shooting up against major international currencies like yen, Indian rupee remains stable”.

IFFCO’s Jordan project starts production

NEW DELHI, Dec 1: IFFCO, World's numero uno cooperative, has reasons to smile. Its mega phosphoric acid joint venture in Jordan has begun commercial production on Monday. NEW DELHI, Dec 1: IFFCO, World's numero uno cooperative, has reasons to smile. Its mega phosphoric acid joint venture in Jordan has begun commercial production on Monday.

IFFCO Managing Director Dr U S Awasthi, who was in Jordan for the Board meeting, tweeted #Congrats to #JIFCO to capitalize Phosphoric Acid project at $860 million. WEF 1st Dec 2014 Board declared start of regular operation. Thanks #JPMC#IFFCO team.

In another tweet, Dr Awasthi said “# Great moment for #IFFCO#JPMC#JIFCO declaring closing & capitalizing of # JIFCO Phosphoric acid project at $860 million.”

IFFCO and Jordan Phosphates Mines Company Ltd (JPMC) had formed a limited liability Joint Venture Company namely Jordan India Fertilizer Company (JIFCO) in 2008. The project is worth $860 million.

The partner of IFFCO, Jordan Phosphate Mines Company (JPMC) owns and operates a large number of phosphate mines in Jordan.

Canara Bank bags Niryat Bandhu award

By Deepak Arora

NEW DELHI, Dec 1: NEW DELHI, Dec 1:

Canara Bank has been conferred with the “Niryat Bandhu” Silver Trophy for the 14th set of Awards in the Banks category.

President Pranab Mukherjee handed over the trophy to Canara Bank Executive Directors V S Krishnakumar.

Every year Federation of Indian Export Organisation (FIEO) organizing “Niryat Bandhu” Award for excellent support services rendered by Banks/other Financial Institutions/Export Promotion councils and Commodity Boards for the promotion of exports.

Canara Banks export credit performance for the past three years has been good. The bank's export Credit outstanding has been Rs 10,382 crore for March 31, 2012; Rs 10,067 crore for March 31,2013, Rs 11,854 crore for March 31,2014 and Rs 11,546 crore for September 30, 2014.

Canara Bank has take several steps to promote export credit. The bank also has competitive advantage Canara Bank to promote export credit.

Canara Bank is giving Thrust to Exports Sector along with other priority sector lending.

The Bank’s pricing on rupee export credit is highly competitive in the industry. The present ROI is 10.70% (Base Rate + 0.5%).

The premium in respect of Post Shipment export credit is being fully borne by the Bank under Whole Turnover Post Shipment Guarantee Cover of ECGC with an intention to encourage exporters to have most of their post shipment dealings with us.

The Bank is conducting Exporters meet at various potential places for improvement of export business as also to get exporter’s feedback.

Canara Bank is providing Gold Card Status to the exporters with good track record as an incentive. |